Owning a home in Toronto comes with its fair share of expenses. Between property taxes, maintenance, and utility bills, the costs add up quickly. One bill that often flies under the radar is your property coverage. Many homeowners pay their premium every year without a second thought. You get the renewal notice in the mail, glance at the total, and let the automatic payment process.

But taking a passive approach to your policy can cost you. The housing market, building costs, and local weather patterns shift constantly, which means Toronto home insurance rates can change over time as well. If you ignore your coverage for too long, you might end up paying significantly more than necessary. Worse, you might not have the right protection when you actually need to file a claim. Let's look at why prices fluctuate and how you can make sure your Toronto home insurance policy actually fits your current needs and budget.

The Problem with Putting Your Policy on Autopilot

Auto-renewing your policy feels like the easiest option. Life is busy, and spending an afternoon reading through coverage limits sounds boring. Because of this, many people let their policies renew automatically for three, five, or even ten years. If you have auto-renewed for three or more years, it is likely time to check your coverage. Insurance companies regularly update their pricing models based on new data. A company that offered the most competitive rate five years ago might no longer be the best fit for your specific property today. When you stay with the same provider indefinitely without checking other options, you miss out on new discounts or better rating systems introduced by competing insurers. Shopping around does not mean you have to switch providers every year. It simply means you are verifying that your current rate makes sense.

What Actually Changes Your Toronto Home Insurance Costs?

Many people assume their premium should stay exactly the same every year unless they make a claim. This is a common misconception. Your individual claims history is just one piece of the puzzle. Insurers look at a wide variety of factors to determine how much risk your property represents.

Neighborhood Risk and Local Events

Where you live in the city plays a massive role in your premium. If your postal code sees a sudden spike in break-ins or property theft, insurance companies take notice. Weather events also heavily influence local rates. Toronto has experienced several severe summer storms and sudden thaws that lead to massive urban flooding. If your specific neighborhood is prone to sewer backups or basement flooding, insurers adjust their prices to reflect that higher risk.

Property Age and Upgrades

Older homes carry different risks than brand-new builds. If your house has original plumbing, outdated electrical wiring, or an older roof, water damage and fire become more likely. Insurers charge more to cover these older systems. On the flip side, if you replace knob-and-tube wiring or install a modern roof, you reduce your risk profile. Your provider needs to know about these updates so they can adjust your premium downward.

Changing Rebuild Costs

Inflation affects everything, including building materials and contractor labor rates. If your house burned to the ground tomorrow, the cost to rebuild it from scratch is likely much higher now than it was five years ago. Insurers routinely adjust coverage limits to ensure you have enough money to rebuild if a total loss occurs. As your coverage limit goes up to match the current cost of lumber and labor, your premium naturally increases to match that higher payout limit.

Life Events That Alter Your Coverage Needs

Your policy should reflect your actual life. As your circumstances change, your protection needs to change alongside them. Major life events often act as natural triggers to review your documents.

Consider reviewing your policy immediately if you experience any of the following changes:

- Moving to a new property: A different house means a different risk profile. The location, size, and age of your new home will completely change your rate.

- Completing major renovations: Finishing your basement, upgrading your kitchen, or adding an extension increases the overall value of your home. If you do not increase your coverage limits to match these upgrades, you could face a major financial shortfall during a claim.

- Buying valuable items: Standard policies put strict limits on how much they pay out for jewelry, fine art, bicycles, or high-end electronics. If you buy an expensive engagement ring or a rare collection, you usually need to add specific coverage for those items.

- Changing your living situation: Renting out a portion of your home or starting a home-based business changes your liability risks. You must inform your provider about these changes to ensure you are actually covered if an accident happens on the property.

How to Tell if You Are Paying Too Much

It is easy to feel entirely disconnected from the insurance process. However, staying informed puts you in a much better position to protect your finances. If you notice your premium creeping up by ten or fifteen percent each year without a clear explanation, you should ask questions.

Call your broker or provider and ask them to explain the increase. Ask if you qualify for any new discounts. Many companies offer lower rates if you install a monitored security system, upgrade your roof, or bundle your home and auto policies together. If they cannot offer a satisfactory explanation or a better rate, it is time to look elsewhere.

You should also check your deductibles. The deductible is the amount of money you agree to pay out of pocket before your coverage kicks in. If your deductible is currently set at $500, raising it to $1,000 or $1,500 can significantly lower your annual premium. You just need to make sure you have that amount set aside in an emergency fund in case something goes wrong.

Practical Steps to Find the Right Coverage

Reviewing your policy does not have to be a painful, time-consuming chore. You can take a few simple steps right now to ensure you are well protected without spending a fortune. First, gather your current documents. Look at the declaration page, which summarizes your limits, deductibles, and annual premium. Understand exactly what you are paying for right now.

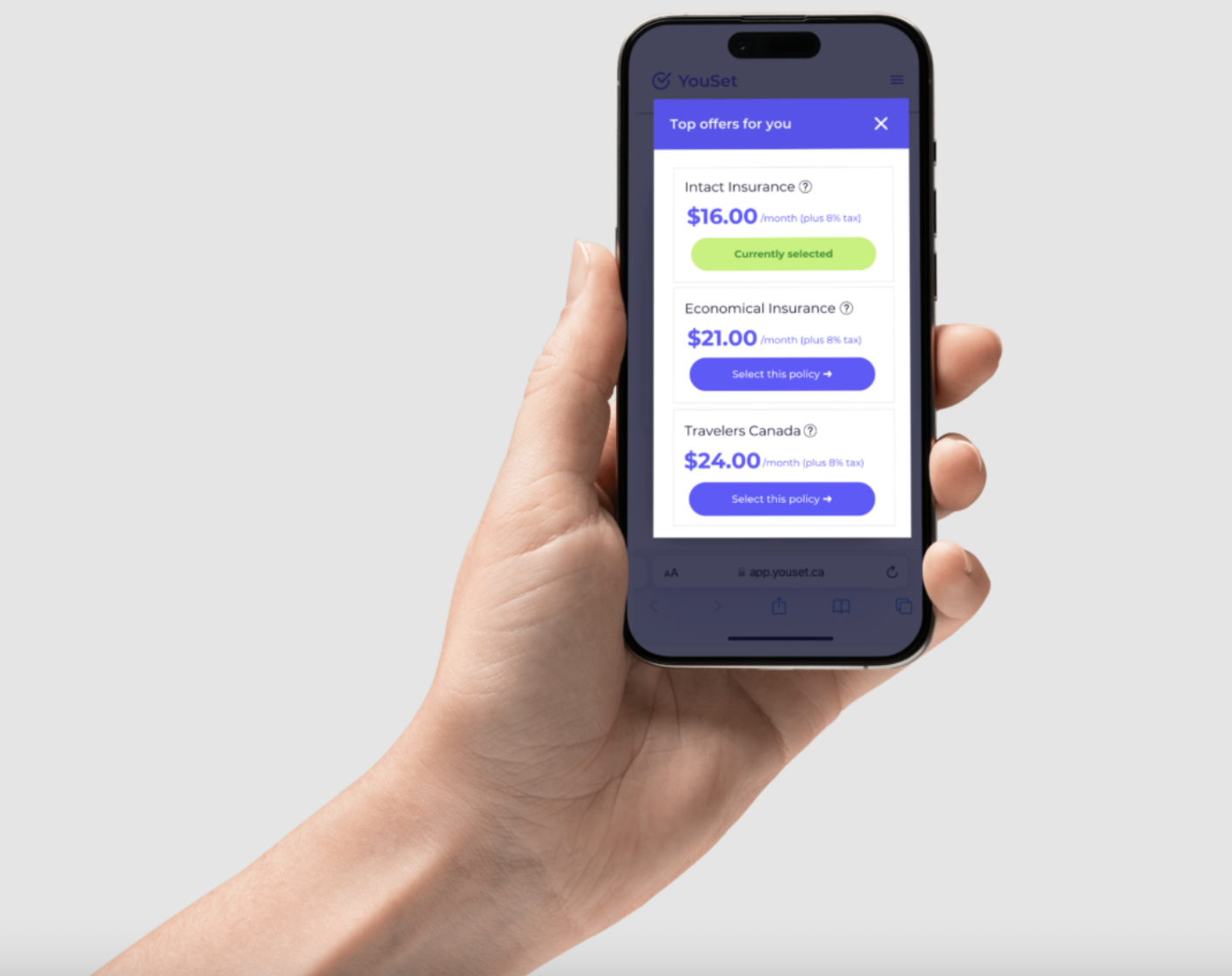

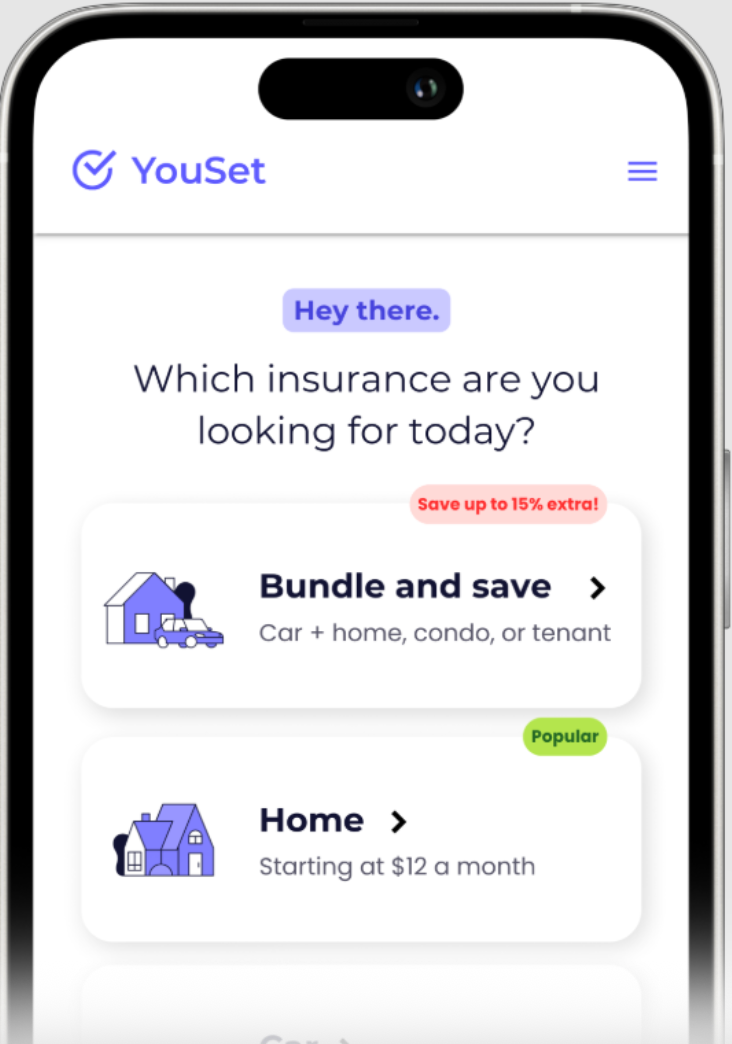

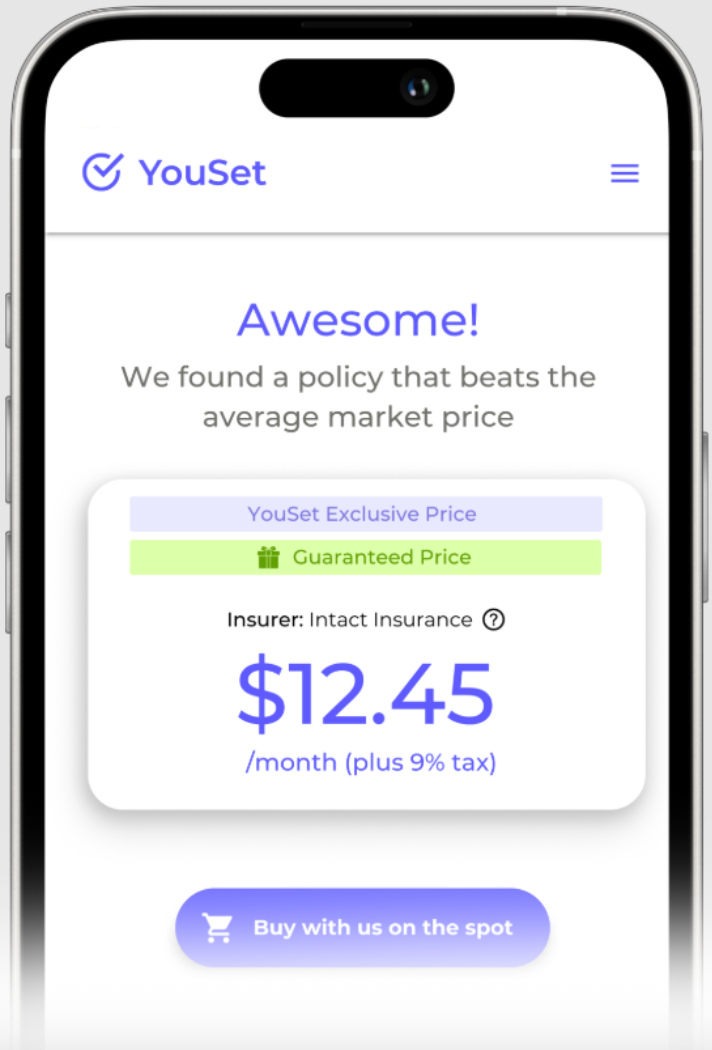

Next, compare prices. You no longer have to spend hours calling ten different brokers and repeating your information over and over. You can use an online insurance platform, like YouSet, to quickly compare quotes from top Ontario insurers. These platforms do the heavy lifting for you, securely checking multiple providers to find the best rate for your specific situation. This ensures you continue getting the best price year after year, often with automatic re-shopping help at renewal time. Finally, do not shop based on price alone. The cheapest policy is useless if it denies your claim when your basement floods. Make sure you compare apples to apples. Check that the new quotes include the same coverage limits, water damage protection, and deductibles as your current policy.

Taking Control of Your Home Expenses

Toronto home insurance is a necessary expense, but you should never pay more than your fair share. By treating your policy as an active part of your financial planning rather than an automatic bill, you keep your money in your pocket. Take ten minutes this week to find your most recent renewal notice. Check how long you have been with your current provider. If it has been a few years, or if your life looks completely different than it did when you first signed those papers, get a few quotes. A quick review might reveal that your current provider is still offering a great deal, giving you peace of mind. Or, you might find out you can save hundreds of dollars a year just by making a simple switch. Either way, taking the time to check is always a smart financial move.